I was chatting with a friend last week who casually mentioned her AI assistant had just reordered her coffee pods. No big deal, right? Except here’s the thing—she didn’t tell it to. The AI noticed her supply was running low, checked her purchase history, found a better price than last time, and completed the transaction. All while she was in a meeting.

That moment? That’s the agentic economy happening right now.

And it’s about to get a whole lot bigger. We’re talking $3-5 trillion by 2030. But here’s the catch—only 16% of US consumers actually trust AI to handle their payments. Meanwhile, companies like Mastercard, Visa, and Google are pouring billions into infrastructure that assumes we’ll all be comfortable with autonomous agents managing our money.

So what’s really happening here? Let me break down what I’ve learned watching this space evolve.

What Are AI Agent Payment Systems? (The Foundation)

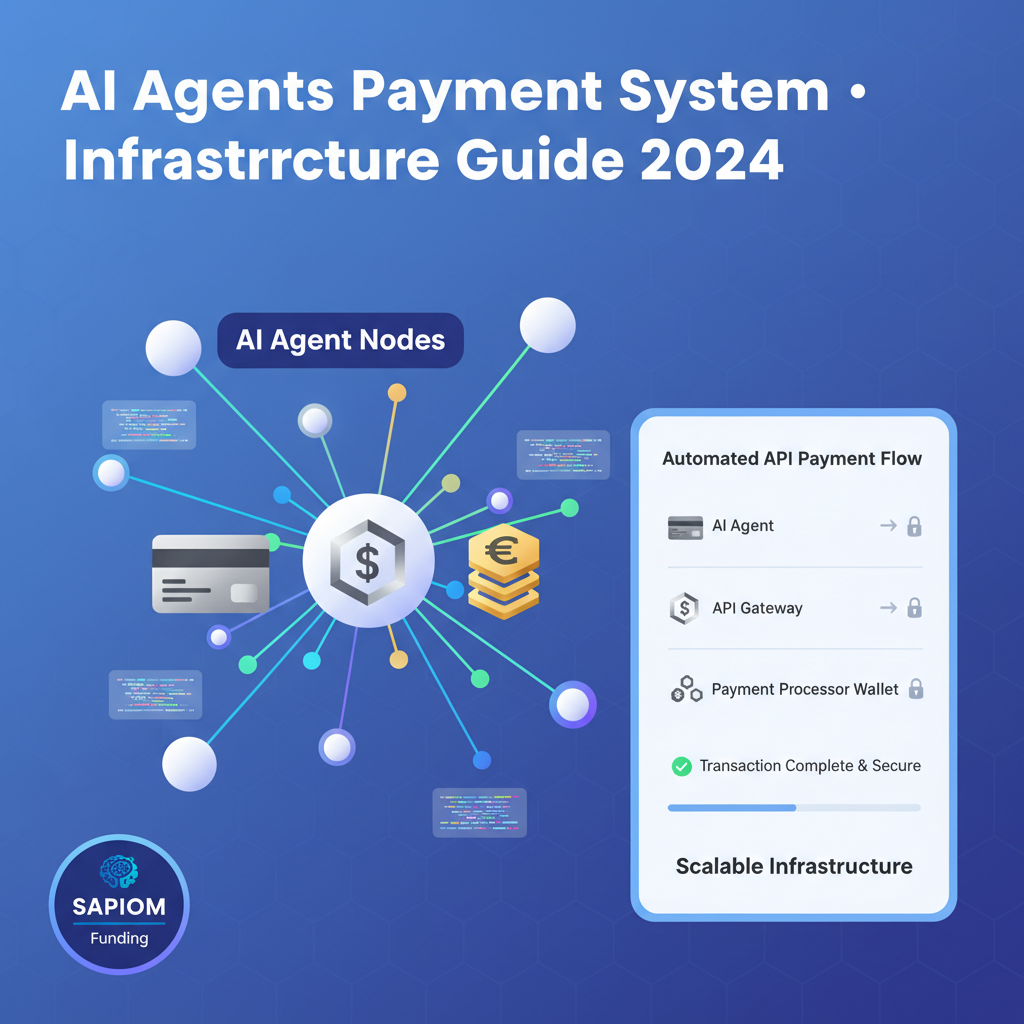

Look, we need to get clear on what we’re actually talking about. AI agent payment systems aren’t just fancy automation tools—they’re fundamentally different from the payment APIs you’re used to.

Traditional payment systems wait for humans to click “buy.” They’re reactive. AI agents? They’re proactive, autonomous software that makes purchasing decisions on your behalf. They evaluate options, negotiate prices, authenticate themselves, and complete transactions without waiting for you to approve every step.

The core components include decision-making algorithms (the brain), authentication protocols (the identity), and payment rails (the actual money movement). But the real shift is this: we’re moving from human-initiated commerce to agent-initiated commerce. That’s a massive psychological and technical leap.

Consider the numbers. ChatGPT alone has 800 million weekly users. Not all of them are shopping, obviously—but that’s the potential market for agent-commerce right there. And 88% of organizations are already using AI in some capacity, which means the infrastructure is being built whether consumers feel ready or not.

Here’s what surprised me: 23% of Americans have already made AI-assisted purchases recently. So despite the trust issues (we’ll get to those), adoption is happening faster than the skepticism would suggest.

Real-World Examples You’re Already Seeing

Google’s “Buy for me” feature lets AI agents purchase items from retailers like Wayfair and Chewy on your behalf. It’s not hypothetical—it’s live. I’ve also seen AI agents booking travel, subscribing to services when they detect you need them, and restocking household items based on usage patterns.

In the enterprise world, procurement agents are autonomously negotiating B2B contracts. They’re analyzing vendor pricing, comparing terms, and executing agreements faster than human procurement teams ever could. It’s honestly kind of wild to watch.

The Explosive Growth of the Agentic Economy ($3-5 Trillion Opportunity)

Okay, let’s talk money. Big money.

The AI agents market in financial services alone is projected to grow from $691.3 million in 2025 to $6.7 billion by 2033. That’s a 31.5% compound annual growth rate, which is—honestly—insane. McKinsey’s projecting the broader agentic commerce market will hit $3-5 trillion by 2030.

But here’s what makes this interesting: the growth isn’t evenly distributed. Fraud detection is currently holding 33.8% of the market share, which tells you where companies are focusing first. They’re solving security problems before they scale the buying side. Smart move, in my opinion.

Gartner says 40% of enterprise applications will include AI agents by the end of 2026. That’s next year. And by 2027, half of all enterprises using generative AI will deploy autonomous agents. The timeline is compressed in ways I haven’t seen with previous technology shifts.

The Numbers That Keep Me Up at Night

One in six Black Friday 2025 purchases were influenced by AI. Not completed by AI necessarily, but influenced. That’s a massive percentage for technology that most people still don’t fully trust.

And get this—23% of organizations are already scaling agentic systems. Not piloting. Scaling. Meanwhile, stablecoin volume grew from $450 billion monthly in 2024 to $710 billion in March 2025. That infrastructure growth is happening because people are preparing for agent-to-agent transactions that need instant settlement.

The geographic breakdown matters too. North America holds 37.8% of the RegTech market share, but Asia’s moving fast. Europe’s taking a more cautious, regulatory-first approach (shocking, I know).

Major Industry Players and 2025 Infrastructure Launches

So who’s actually building this stuff?

Mastercard and Visa aren’t sitting around waiting to see what happens. They’re launching agent-specific payment solutions designed for the unique demands of autonomous transactions. Mastercard’s working on tokenization systems for agent wallets—basically, giving AI agents their own secure payment credentials.

Visa’s focused on real-time settlement protocols because agents don’t want to wait three business days for transactions to clear. When an AI needs to purchase GPU time or API credits, it needs that settlement now. Not tomorrow.

Google’s “Buy for me” feature is probably the most visible consumer-facing implementation. They’ve integrated with major retail partners, and honestly, it’s smoother than I expected. The AI can compare prices, check inventory, and complete purchases across multiple retailers without you opening a dozen browser tabs.

Oracle launched their Investigation Hub in March 2025, which is specifically designed for financial crime automation. Because here’s the thing—when you have autonomous agents making millions of micro-transactions, traditional fraud detection falls apart. You need AI investigating AI, which feels very sci-fi but is absolutely necessary.

What Banks Are Actually Doing

Banks are targeting scale deployment in 2026. And 93% of IT leaders are planning autonomous agent deployment, which means the infrastructure investments are happening right now. IDC projects that 26% of the $1.3 trillion global IT spend will go toward agentic AI by 2029.

That’s not a rounding error. That’s a fundamental reallocation of technology budgets.

The Trust Deficit: Why Only 16% of Consumers Trust AI Payments

Here’s where things get complicated.

Only 16% of US consumers trust AI for payments. In the UK, it’s slightly better at 29%, but that’s still less than a third. Yet—and this is the paradox—23% of Americans have already made AI-assisted purchases. So people are using technology they don’t trust. That’s… not sustainable.

I’ve talked to dozens of people about this, and the concerns are pretty consistent: security (what if it gets hacked?), loss of control (what if it buys something I don’t want?), transparency (how did it make that decision?), and accountability (who’s responsible when it screws up?).

The psychological barrier is real. Delegating spending authority to software feels fundamentally different than using software to execute a purchase you’ve already decided to make. It’s the difference between a calculator and a financial advisor—except the advisor is an algorithm that never sleeps.

Building Trust (Or Trying To)

Companies are trying different approaches. Transparency dashboards that show agent decision-making logic. Multi-factor authentication for high-value transactions. Spending limits and approval workflows that let you maintain oversight without micromanaging every purchase.

Some are implementing explainable AI in payment decisions—basically, the agent has to show its work. And I’ve even seen insurance products emerging for agent transaction errors, which is both reassuring and slightly terrifying.

But honestly? I think trust will follow utility. As people see agents making better purchasing decisions than they would’ve made manually—finding better prices, better timing, better options—the trust will build. It’s just going to take time.

Infrastructure Requirements for Agent-to-Agent Transactions

This is where it gets technically interesting.

Agent-to-agent transactions have completely different requirements than human-to-business transactions. You need real-time metering capabilities because agents might be purchasing resources by the millisecond. Per-token pricing for language models, per-API call for services, per-GPU-second for compute resources.

Traditional payment rails weren’t built for this. They were built for discrete transactions—you buy a thing, money moves, transaction complete. But when an AI agent is dynamically purchasing and selling resources in real-time, you need instant settlement. Batch processing doesn’t cut it.

That’s where programmable money and smart contracts come in. You can embed payment logic directly into the transaction itself. The money knows what it’s supposed to do and executes automatically when conditions are met.

The Interoperability Challenge

Here’s what keeps infrastructure engineers up at night: interoperability. When an OpenAI agent needs to pay a Google Cloud agent which needs to pay an AWS agent, they all need to speak the same payment language. Right now, we don’t have universal standards for that.

Stablecoin volumes growing from $450 billion to $710 billion monthly tells you where some of the infrastructure is heading—crypto rails for instant cross-border settlements. And with AI task capabilities doubling every seven months, the infrastructure demands are accelerating faster than traditional financial systems can adapt.

The practical examples are everywhere now. OpenAI’s API credits with per-token billing. Cloud GPU rental markets with sub-second billing cycles. Agent marketplaces where AI agents purchase skills, data licenses, or specialized capabilities from other agents. It’s a whole economy that barely existed two years ago.

Regulatory Compliance and the $14 Billion Non-Compliance Problem

Let’s talk about everyone’s favorite topic: regulations.

The regulatory landscape for autonomous payments is—how do I put this delicately—a mess. Because the regulations were written for humans making decisions, not algorithms. KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements assume there’s a customer to know. But what’s the identity of an AI agent?

And liability frameworks are even murkier. If an agent makes an illegal transaction, who’s responsible? The person who deployed it? The company that built it? The agent itself? (Spoiler: not the agent, it’s software.)

Companies are facing $14 billion in non-compliance costs, which is driving massive RegTech adoption. The RegTech market is projected to exceed $22 billion by 2026, and a huge chunk of that is specifically addressing autonomous transaction compliance.

What Compliance Actually Looks Like

Oracle’s Investigation Hub is one approach—using AI to monitor AI. Automated suspicious activity reporting. Transaction monitoring systems that look for patterns in agent behavior that might indicate fraud or money laundering.

Some companies are implementing agent identity verification protocols—basically, digital passports for AI agents that carry compliance credentials. Others are embedding regulatory rules directly into smart contracts, so the payment literally can’t execute if it violates compliance requirements.

Cross-border compliance automation is particularly interesting because agents don’t think in terms of jurisdictions. They just see resources to purchase. But the legal reality is that moving money across borders triggers different regulatory requirements in different countries. Automating that compliance is complex but necessary.

Strategic Roadmap: Preparing Your Business for Agent Payments (2026-2030)

So what should you actually do about all this?

First, assess where you are. Can your current payment infrastructure handle micro-transactions? Real-time settlements? Agent authentication? If the answer’s no (and for most businesses, it is), you need to start planning infrastructure investments now.

Partnership strategies matter more than building everything yourself. Unless you’re a massive enterprise with unlimited resources, you’ll want fintech partners and payment processors who’ve already solved these problems. Mastercard and Visa aren’t building their agent payment solutions for fun—they’re building them because they know businesses will need them.

Start Small, Think Big

Design pilot programs that test specific use cases. Maybe start with internal procurement—let an AI agent handle office supply reordering. Low risk, measurable results, clear ROI. Then expand from there.

Risk management and governance structures are non-negotiable. You need clear policies on agent spending limits, approval workflows, and override capabilities. Because at some point, an agent will make a decision you disagree with, and you need mechanisms to handle that.

Timeline-wise? If you’re not running pilots by mid-2026, you’re behind. By 2027, this won’t be experimental—it’ll be expected. And by 2030, businesses without agent payment capabilities will be at a significant competitive disadvantage.

The 40% of enterprise apps that’ll include AI agents by end of 2026 aren’t all going to be read-only. They’ll need to transact. They’ll need to purchase resources, subscribe to services, pay for data. Your business needs to be ready to accept those payments—and potentially deploy agents that make them.

The Bottom Line

Look, I get the hesitation. Letting AI handle your money feels like a big leap. But the infrastructure is being built, the market opportunity is massive, and the timeline is compressed. Whether you’re ready or not, agent payments are coming.

The businesses that figure this out early—that build trust with customers, invest in the right infrastructure, navigate the regulatory complexity—they’re going to have a significant advantage. The ones that wait until it’s fully mainstream? They’ll be playing catch-up in a market that moves faster than traditional payment systems ever did.

The agentic economy isn’t a distant future. It’s happening now. The question isn’t whether to prepare—it’s how quickly you can move.

Ready to take your payment infrastructure to the next level? Contact our experts for personalized guidance on implementing AI agent payment systems for your business.